5 Corporate Onboarding Best Practices for 2026 [Explained]

Date

Author

Highnote Team

Corporate onboarding is an essential but complex process for mid-sized financial institutions. Regulatory pressure, stricter beneficial ownership transparency requirements, and rising client expectations force organisations to do more with fewer resources.

In addition to collecting documents, organisations have to run identity verification, customer due diligence, risk assessment, sanctions screening, and ongoing monitoring, all while providing a smooth experience for clients.

Without the right approach, the whole process becomes overwhelming and increases the risk of mistakes that can lead to compliance and regulatory issues.

Read on to learn more about corporate onboarding best practices that can help you improve efficiency without compromising on regulatory standards or compliance.

Key takeaways

Strong corporate onboarding starts with accurate customer identification

A robust Customer Identification Program (CIP) helps verify not only the business itself but also its directors, shareholders, and Ultimate Beneficial Owners (UBOs). Without reliable identification, risk assessments, screening, and ongoing monitoring become less effective.Customer Due Diligence (CDD) is essential for understanding risk

CDD helps organisations understand the source of funds, business activities, and expected transaction patterns. This information is essential for customer risk ratings, and it can help you detect unusual or potentially suspicious behaviour later in the relationship.Corporate onboarding doesn't end once a customer is approved

Ongoing risk assessments, sanctions monitoring, and audit trail maintenance are just as important as the initial onboarding. Customer risk profiles can change over time, making continuous monitoring essential for staying compliant and identifying emerging risks.A unified compliance platform reduces onboarding complexity

Instead of managing multiple tools, spreadsheets, and disconnected workflows, Trustform brings onboarding, KYB verification, ownership mapping, risk assessment, ongoing due diligence, monitoring, and audit management into a single system. This helps mid-sized financial institutions onboard complex corporate clients faster while maintaining transparency, regulatory compliance, and audit readiness.

Corporate onboarding challenges

Mid-sized companies face challenges that enterprises don't encounter in the same way.

Regulatory pressure has increased with the implementation of EU AML directives, the Fifth Money Laundering Directive (5MLD), and stricter requirements for beneficial ownership transparency.

For European mid-sized businesses, alignment with these directives and local regulatory blacklists is non-negotiable.

In addition, mid-sized businesses must meet the same compliance standards as enterprise banks, but with resources that are usually much more limited.

All of the above have contributed to already complex onboarding challenges:

Manual processes causing delays: Institutions still rely on paper documentation, manual data entry, spreadsheet-based tracking, and fragmented tools, which can stretch onboarding into weeks.

High false positives in screening: Without intelligent automation, name screening systems label legitimate customers as sanctions list matches because of minor name similarities, resulting in manual review that delays onboarding.

Complex beneficial ownership structures: Corporate structures with offshore holdings, multi-layered ownership chains, and circular ownership patterns can hide UBOs, which makes it harder to comply with regulatory bodies that demand precise, clear identification.

Balancing compliance with customer experience: Every compliance check can slow onboarding, but removing checks creates regulatory risk. Mid-sized businesses often struggle to find the right balance where compliance is thorough but doesn't feel burdensome to customers.

5 corporate onboarding best practices mid-sized businesses should know about

Despite these challenges, there are practices and processes that highly regulated companies can implement to handle the onboarding complexity in more customer-centric but compliant ways.

Here are the key ones:

Best practice | What it involves | Why it’s important |

Implement a Customer Identification Program | Verifying the customer’s identity and collecting beneficial ownership information | Ensures all downstream compliance activities are based on accurate customer identity and ownership data |

Conduct Customer Due Diligence | Understanding the customer’s business purpose, source of funds, and expected transaction patterns | Enables accurate risk classification and helps detect unusual or suspicious activity based on defined customer behaviour |

Apply Enhanced Due Diligence (EDD) for high-risk customers | Applying deeper checks for high-risk customers such as PEPs, cross-border entities, and adverse media cases | Provides stronger scrutiny for higher-risk relationships and helps verify the legitimacy of wealth |

Implement real-time sanctions screening | Using continuously updated sanctions and watchlist data via automated or API-based screening | Ensures immediate detection of sanctioned entities and prevents onboarding or continued engagement with restricted customers |

Map ownership structures automatically | Identifying and visualising directors, shareholders, UBOs, and connected entities across corporate structures without manual diagramming | Improves transparency of complex ownership arrangements, reduces manual effort, and helps compliance teams quickly identify ultimate control and potential hidden risk exposure |

1. Implement a Customer Identification Program

Establishing and verifying the customer's identity is the first step in the onboarding process.

Also, the Financial Action Task Force (FATF) emphasises that customer identification must be confirmed through reliable verification methods.

Without accurate identification, all subsequent compliance measures, such as screening, risk assessment, and monitoring, become ineffective because you're not sure who you're actually assessing.

To implement CIP for entities, you must collect beneficial ownership information. You have to identify not just the company but the natural persons who ultimately own or control it.

For example, with Trustform, you can manage all entities and stakeholders, and you can add and track key relationships such as:

Authorised persons

Controlling persons

Directors

Shareholders

Ultimate Beneficial Owners (UBOs)

All corporate client information is collected in a single guided flow, so you stay compliant with regulatory requirements while maintaining a complete view of every relevant relationship.

2. Conduct Customer Due Diligence

CIP tells you who the customer is, while CDD tells you what they're doing and why. It allows you to understand the customer's nature, the purpose of the relationship, and the risk profile.

CDD is important because financial crime often involves transactions inconsistent with legitimate business purposes. Without it, you can't assess whether transactions are suspicious because you don't know what's ‘normal’ for that customer.

What you must document:

Source of funds: To identify whether funds have legitimate origins, you need to know the origin of the customer's money, their salaries, business revenues, investment returns, and loans.

Nature of business: Different business types, such as manufacturing, consulting, or retail, have different risk profiles, and understanding the business and what it actually does helps you identify unusual transaction patterns.

Expected transaction patterns: A consulting firm should have different transaction patterns from a retail business. Documenting expectations is the basis for ongoing monitoring and identifying suspicious behaviour.

Compliance requirements: You should maintain a well-documented CIP as part of an AML compliance programme so that regulators can review it when needed.

Risk assessment: The information collected during CDD is the primary factor used to classify customers as low-, medium-, or high-risk.

Worth knowing:

Trustform centralises customer due diligence into a unified workflow that combines onboarding, verification, screening, monitoring, reviews, and audit tracking, which helps compliance teams move faster while maintaining regulatory oversight.

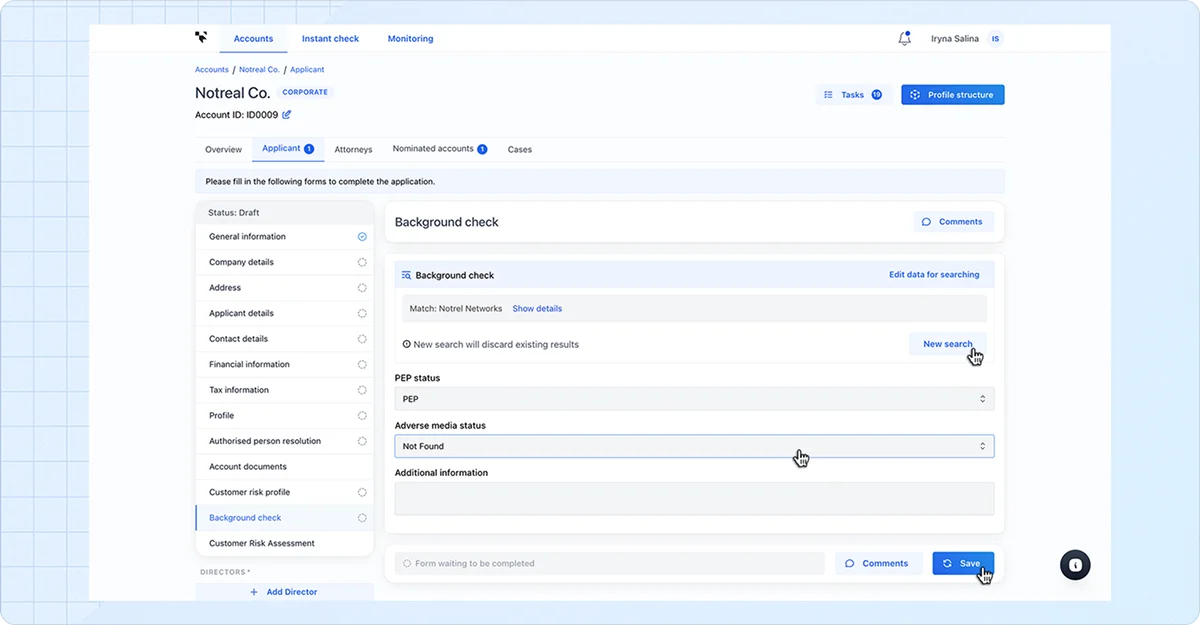

3. Apply Enhanced Due Diligence for high-risk customers

EDD isn’t always necessary, but it applies to specifically identified high-risk categories:

Politically Exposed Persons (PEPs): Individuals who hold or have held prominent public positions, their family members, and close associates

Cross-border entities: Companies operating across multiple jurisdictions, especially those involving countries with weak AML controls

Adverse media cases: Customers identified through negative news screenings as involved in financial crime, corruption, fraud, or other illegal activities

EDD builds on CDD by offering a broader, deeper view of the customer's overall wealth accumulation history, which helps identify whether that wealth has legitimate origins or results from illicit activities.

Also, EDD cases require explicit approval from senior management or the compliance officer, not just automated system approval. This way, human oversight for high-risk cases is ensured, with accountability at the executive level.

Worth knowing:

Trustform checks against connected sanctions lists, PEP databases, and adverse media sources, showing you all potential matches filtered by entity type, country, and date of birth.

You can also set the PEP status, adverse media status, and add additional information before running the new screening.

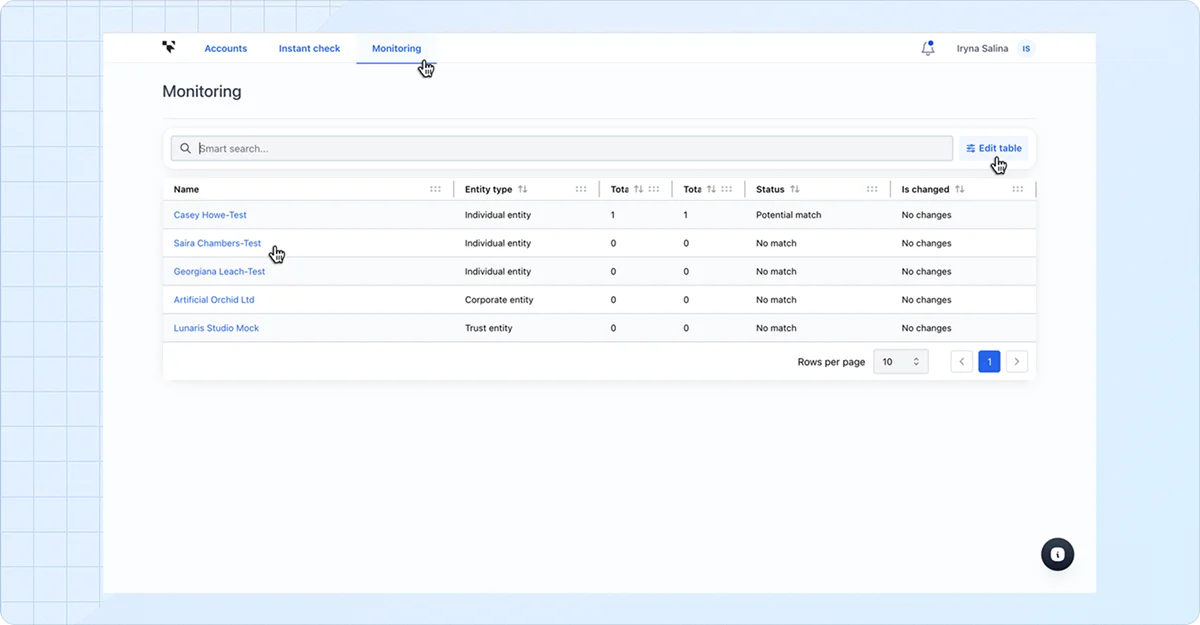

4. Implement real-time sanctions screening

Traditional manual screening against static list downloads creates delays and may become outdated.

On the other hand, API-based cross-checking runs screening against constantly updated multiple sanctions and watchlist databases such as the US Office of Foreign Assets Control (OFAC), UN sanctions lists, EU sanctions, and local regulatory blacklists, which are country-specific.

API integration enables:

Real-time results: Screening happens instantly during onboarding, not days later.

Automatic updates: Lists refresh automatically as sanctions change.

Scalability: You can screen thousands of customers without additional staff.

Integration: Screening is embedded directly in the onboarding workflow, so compliance checks run constantly as part of the core process.

This way, organisations can achieve faster onboarding and operational efficiency while maintaining compliant screening.

Keep in mind that you can’t onboard customers who appear on sanctions lists, as this is a legal requirement in most jurisdictions and carries severe penalties for violations.

Worth knowing:

Trustform automatically and continuously screens all active clients and associated entities. As a result, you are instantly notified of any new risks, enabling you to maintain compliance oversight.

5. Map ownership structures automatically

Complex corporate ownership is one of the biggest challenges in KYB onboarding. Businesses may be registered across multiple jurisdictions, ownership can be split across several entities, and control can be hidden through indirect or circular arrangements.

In these cases, understanding who ultimately owns or controls an entity is essential for meeting AML and compliance requirements.

However, this is often difficult to achieve using manual processes.

Automated ownership mapping solves this by bringing all relevant corporate relationships into a single, structured view. Instead of manually building diagrams or reviewing fragmented documents, compliance teams can see directors, shareholders, UBOs, and authorised persons in one place.

Compliance platforms achieve this by connecting corporate data sources directly into the onboarding workflow and automatically linking related entities based on verified registry and identity data.

This way, changes in shareholders or directors are immediately reflected without manual updates.

Worth knowing:

Trustform brings all key corporate information into a single client profile, where ownership structures are automatically visualised and kept up to date throughout the onboarding process.

Because the ownership view is embedded within a broader onboarding flow, KYB verification, risk assessment, and review processes remain connected to the same underlying data.

2 major post-onboarding practices you shouldn’t miss

If you focus only on onboarding practices and ignore post-onboarding, your risk classification may become outdated as customer behaviour changes. This means that financial crime may go undetected because monitoring doesn’t prompt reassessments.

In addition, regulatory exams can fail because of poor record maintenance, and you may lose audit trail data when systems change.

Below are two major post-onboarding practices:

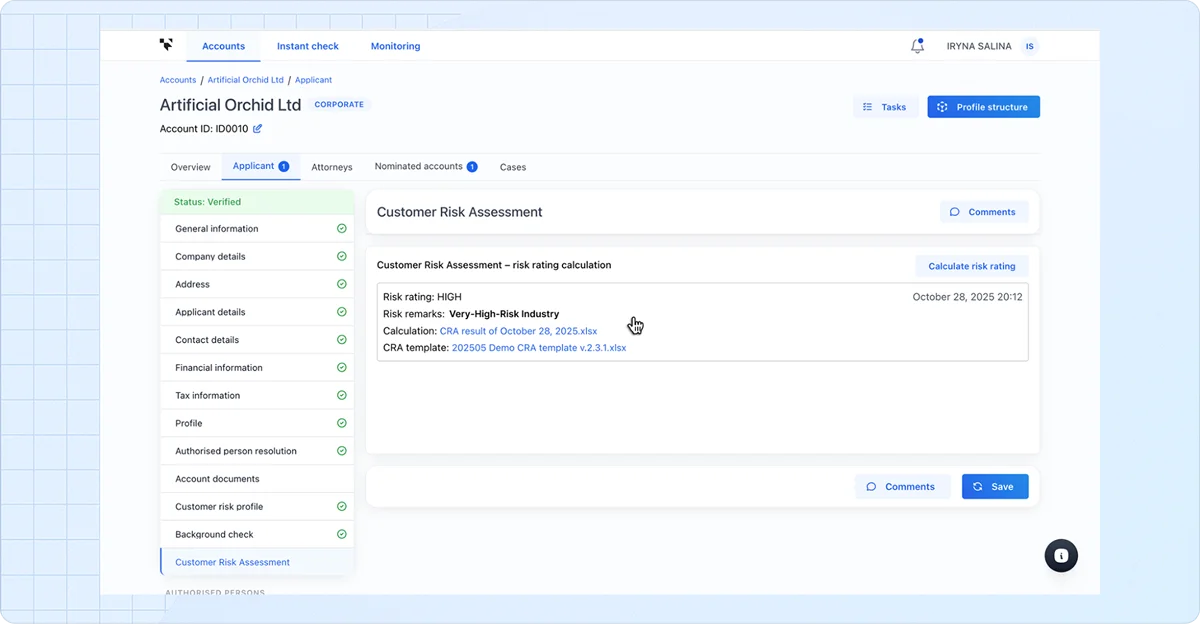

1. Continue with risk assessment

You should continue to evaluate and update the customer's risk level based on their actual transaction behaviour, not just the information you collected during onboarding.

You must reassess the customer's risk level when monitoring detects important anomalies, such as:

Sudden volume spikes: A customer normally processes 10 transactions per month, but the volume suddenly jumps to 50.

New counterparty types: A manufacturing company starts transacting with cryptocurrency exchanges.

Geographic changes: A domestic business suddenly starts engaging in frequent transactions with high-risk countries.

Timing anomalies: Transactions start happening at unusual hours, for example, 3 AM for a business that operates 9–5.

Worth knowing:

Trustform automatically calculates and assigns client risk levels during the onboarding process in accordance with your company’s risk management policies and based on the criteria defined in the CRA template.

We provide separate CRA templates for each client type: individual, corporate, trust, or partnership.

In addition, you can evaluate a client’s risk level at any point, not just during onboarding.

2. Maintain audit trail

During onboarding, you create the initial audit trail by documenting all steps, attaching documents to customer profiles, and saving monitoring configurations.

After onboarding, you must continuously maintain these trails by adding new records, including transaction monitoring alerts, risk reassessments, and customer updates, to ensure the system remains searchable and accessible.

You should keep all records for 5–7 years, depending on jurisdiction. This includes:

Original onboarding records: CIP, CDD, EDD, screening results

Post-onboarding records: Monitoring alerts, risk reassessments, annual reviews

System records: Access logs, document version history

The audit trail structure you created during onboarding impacts how easily you can maintain records afterwards. If you didn’t tag documents properly during onboarding, post-onboarding maintenance becomes error-prone.

How to do corporate onboarding efficiently with Trustform

Trustform is an end-to-end compliance orchestration platform that unifies complex corporate onboarding and risk assessment, ongoing due diligence, and transaction monitoring.

For businesses that use Trustform directly, the platform enables them to maintain ownership of their compliance profile and keep a verified business identity that updates as changes happen.

On the other hand, companies interacting with businesses using Trustform can request and receive verified information through a controlled, standardised process, without relying on fragmented onboarding workflows or repeated manual checks.

For companies operating across multiple entities or platforms, our Portable KYB solution enables profile reuse, which simplifies onboarding and supports ongoing compliance and regulatory reviews.

Regardless of the use case, granular data-sharing controls allow businesses to decide exactly what information to disclose, approve each request, and share additional details only when necessary.

With Trustform, you can:

Capture company information, ownership data, documents, verification results, and risk insights in a unified workflow

Have all the information connected across verification, screening, review, and approval processes

Automatically visualise directors, shareholders, UBOs, and authorised persons within complex corporate structures

Verify corporate entities during onboarding while capturing registration data, legal status, and key company identifiers

Calculate client risk using configurable methodologies and automatically reassess risk when information changes

Automatically record checks, communications, decisions, and approvals

Curious to know more?

Book a demo today to see how you can onboard complex corporate clients faster while maintaining transparency, consistency, and audit readiness.

FAQ:

1. How do mid-sized businesses manage corporate onboarding?

Mid-sized businesses usually manage corporate onboarding through a combination of KYB verification, ownership structure reviews, risk assessments, and compliance checks.

Companies look for digital onboarding platforms that automate data collection, ownership mapping, screening, and approval workflows, so they can onboard corporate clients faster while maintaining regulatory compliance and reducing manual effort.

2. What challenges do businesses face during corporate onboarding?

Corporate onboarding can be complicated because of complex ownership structures, incomplete documentation, manual data collection, and evolving regulatory requirements.

These challenges often lead to delays, increased compliance risks, and a poor customer experience if not managed through standardised and automated processes.

3. Why is corporate onboarding important for compliance?

Corporate onboarding helps organisations verify the identity, ownership, and risk profile of business customers before establishing a relationship.

A robust onboarding process supports AML, KYC, and KYB compliance requirements, reduces exposure to financial crime, and creates a strong basis for ongoing due diligence and monitoring.